- Daily Update from Securities Docket

- Posts

- SEC Director of Enforcement David Woodcock Shares How He Intends to Lead the Division

SEC Director of Enforcement David Woodcock Shares How He Intends to Lead the Division

Plus the "greatest comment letter in the history of SEC comment letters."

Bruce Carton

May 14, 2026

SPONSORED BY

Good morning! Here’s what’s up.

Clips ✂️

David Woodcock’s Remarks at the MFA Legal & Compliance 2026 Conference

Today, I want to share a bit about how I intend to lead the Division.

Simply put, my role is to ensure that our staff are empowered, supported, and equipped to execute the Commission’s mission. I intend to provide hands-on leadership that allows our teams to focus on the fundamentals – the blocking and tackling if you will, with professionalism, efficiency, and fairness. In doing so, I am committed to ensuring the Division remains the global gold standard in securities law enforcement.

As a matter of first principles, my goals are aligned to those of Chairman Atkins: to return the enforcement program back to basics. That means vigorously protecting investors and safeguarding markets, while also providing transparency and certainty to those we regulate.

A quick aside, there has been considerable attention paid to the decline in the number of cases brought over the last several years. Let me be clear: this Commission has deliberately shifted toward an emphasis on quality over quantity, and I fully support that direction.

Our focus is, and will remain, on protecting investors and safeguarding markets from real harm. That means identifying and stopping fraud and manipulation in all its forms—for instance, offering frauds, accounting and disclosure fraud, insider trading, market manipulation, fraud by foreign actors targeting U.S. markets and investors, and breaches of fiduciary duties by advisers misusing client assets.

These are the types of cases contemplated when the Division was created, and these are the cases the Division intends to pursue aggressively during my tenure.

Several recent matters reflect this focus on addressing the most harmful misconduct.

👉 Great to see new SEC Director of Enforcement David Woodcock already out discussing his plans and vision for the enforcement program — just a week after starting in the position!

Judge Says Cannot ‘Rubber Stamp’ $1.5 Million Musk-SEC Deal

A federal judge cited “red flags” about a proposed $1.5 million deal between Elon Musk and the Securities and Exchange Commission to end the agency’s lawsuit alleging the world’s richest person waited too long in 2022 to reveal his growing stake in Twitter Inc.

“I am not going to rubber stamp this settlement and I cannot rubber stamp this settlement,” US District Judge Sparkle Sooknanan said on Wednesday, adding that details in the proposed settlement “raise red flags for me.”

Sooknanan ordered attorneys for Musk and the SEC to answer questions by June 1 about how the parties reached the deal, including why the proposed settlement involves a trust tied to Musk instead of the billionaire himself.

“Is Mr. Musk getting some kind of special treatment in this case?” she asked.

👉 As discussed in this WSJ article:

Sooknanan explained she is required by court precedent to review the agreement for fairness and reasonableness and in doing so noticed irregularities. She questioned why the SEC was fining the trust and not Musk personally, which she said “seems strange,” and why the agency decided to drop its demand for Musk to pay back his alleged ill gotten gains.

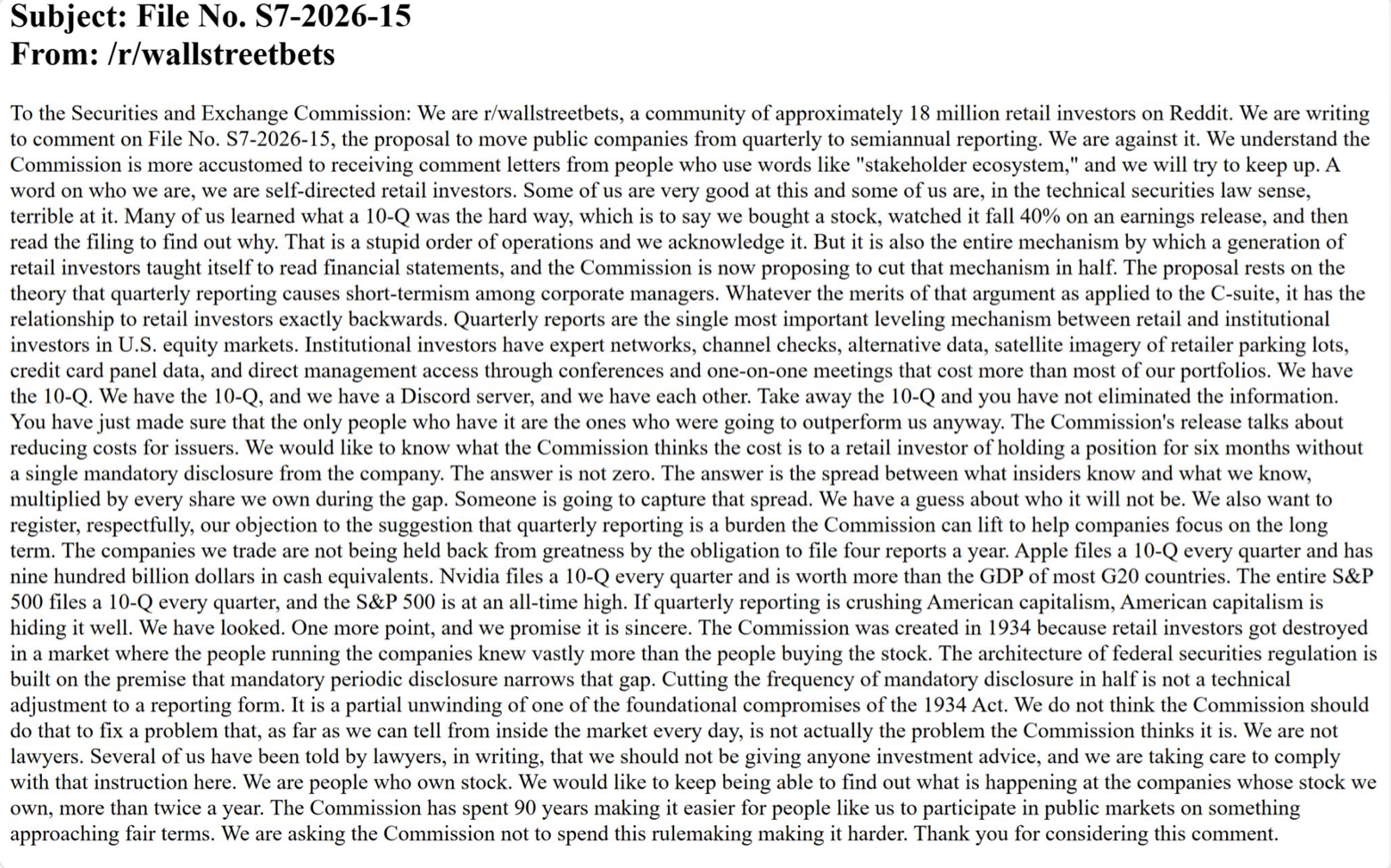

Meme Stock Redditors Weigh In Against Semiannual Reporting Shift

WallStreetBets has entered the chat.

The Reddit-based retail investor community famous for launching the meme-stock phenomenon filed a public comment Tuesday opposing a proposed shift to semiannual, rather than quarterly, securities reports. Securities and Exchange Commission Chairman Paul Atkins unveiled the fast-tracked plan after President Donald Trump called for an end to decades-old rules mandating quarterly filing of the public disclosures known as 10-Qs.

“Many of us learned what a 10-Q was the hard way, which is to say we bought a stock, watched it fall 40% on an earnings release, and then read the filing to find out why,” the WallStreetBets filing says. “That is a stupid order of operations and we acknowledge it. But it is also the entire mechanism by which a generation of retail investors taught itself to read financial statements, and the Commission is now proposing to cut that mechanism in half.” […]

“If quarterly reporting is crushing American capitalism, American capitalism is hiding it well,” the comment says. “The Commission has spent 90 years making it easier for people like us to participate in public markets on something approaching fair terms. We are asking the Commission not to spend this rulemaking making it harder.”

👉 The full comment is here.

The comment is extraordinary enough that two of you sent it to me immediately (thank you). Alex Rapp posted it on LinkedIn with the caption, “I respectfully submit that this is the greatest comment letter in the history of SEC comment letters” — to which a number of commenters responded with the type of superlatives usually reserved for the hype comments on a new book (“Brilliant!” … “Fascinating and well-written!” … “Finest ever”).

I agree it is a thoughtful and well-written comment but I cannot support “greatest comment letter” status to something that is presented to the reader like this:

C’mon man! Just hit “Return” on the keyboard a couple times!

Self-report fraud and walk free, New York prosecutors tell Wall Street

Wall Street’s top prosecutors want lawbreaking companies to hand themselves in, offering behind-closed-door deals that let them avoid being charged, fined or having full details of their fraud made public.

The US Attorney’s Office for the Southern District of New York, which secured huge fines and guilty pleas from companies such as Drexel Burnham Lambert and Steve Cohen’s SAC Capital, has been meeting big law firms and corporate advisers in recent weeks to promote its softer approach to white-collar crime.

The lenient new deals are available even in cases where alleged fraud was pervasive, caused severe harm, involved senior leaders and had already been reported in the press or by a whistleblower.

Corporate Risk Leaders Flag Mounting Threats Across the Board—And Aren’t Ready for Most of Them

A new survey of 500 senior U.S. legal, compliance and risk executives finds widespread concern about rising corporate litigation, fragmented AI regulation, and cybersecurity threats, but significant gaps in organizational readiness to address them.

Released Wednesday by global consulting firm AlixPartners, the 2026 U.S. Risk Survey found that more than 60% of respondents expect corporate disputes to increase this year. The survey defines corporate disputes as commercial litigation and arbitration outside of government regulatory actions, and attributes the expected rise to economic volatility, AI-driven upheaval, and whipsawing trade policy.

Eight in 10 respondents said the federal government’s evolving—and increasingly permissive—approach to AI policy poses a strategic risk to their compliance programs as the regulatory landscape grows more fragmented.

👉 AlixPartners’ 2026 U.S. Risk Survey is here.

Job Posting of the Day Year

Who wants to be General Counsel of Stanford University?